How to Run Finances in a Startup

Fibery is an all-in-one task and knowledge management tool for product companies, and when we say all-in-one, we mean it. We run all our operations, including financial ones, in Fibery. Before any tool there is a process, often not an obvious one. In a series of articles based on the blood and tears of our COO Katsiaryna, we will share how to approach financial operations in a product startup - and how to set it up in Fibery.

Intro

I have been helping to set up new businesses for the last 15 years.

I clearly recall the first frustration of dealing with an accountant - all the joy from the sales achievements in the first startup I worked for was disrupted by the accountant’s request for the documents to calculate cost price, revenue, and VAT as the quarter had ended.

The frustration persisted as the businesses changed, even when finance management became my key responsibility. Whether it was agriculture, leadership training, real estate, or software development, the challenges remained the same.

After joining Fibery, I realized how much easier the bureaucratic process could have been. All the pivot tables, reports, and complex connections between them can be handled in one tool without spending tens of thousands of dollars on maintaining complex IT infrastructure. It’s a relief!

Let’s start from the basics, though.

How to turn a product startup into a legal business

We all know that the most important things in a startup are the idea and the product. You need to come up with an innovative idea, conduct thorough research to understand the market and customers, assemble a team, and develop a minimum viable product (MVP). It feels like the majority of all books and motivational speeches are focused on these aspects.

Right after you have made this massive effort and succeeded, the boring reality kicks in.

Now, you need to make your business legal and operational.

This means you need to:

- Decide on the type of legal entity.

- Select a unique name to ensure it complies with local naming conventions and does not infringe on any existing trademarks.

- Choose the jurisdiction and register your entity with the relevant government authorities.

- Determine if your startup requires any specific licenses or permits to operate legally.

- Register your entity for tax purposes.

- Prepare and draft essential legal documents for your startup.

- Understand and comply with employment laws and regulations.

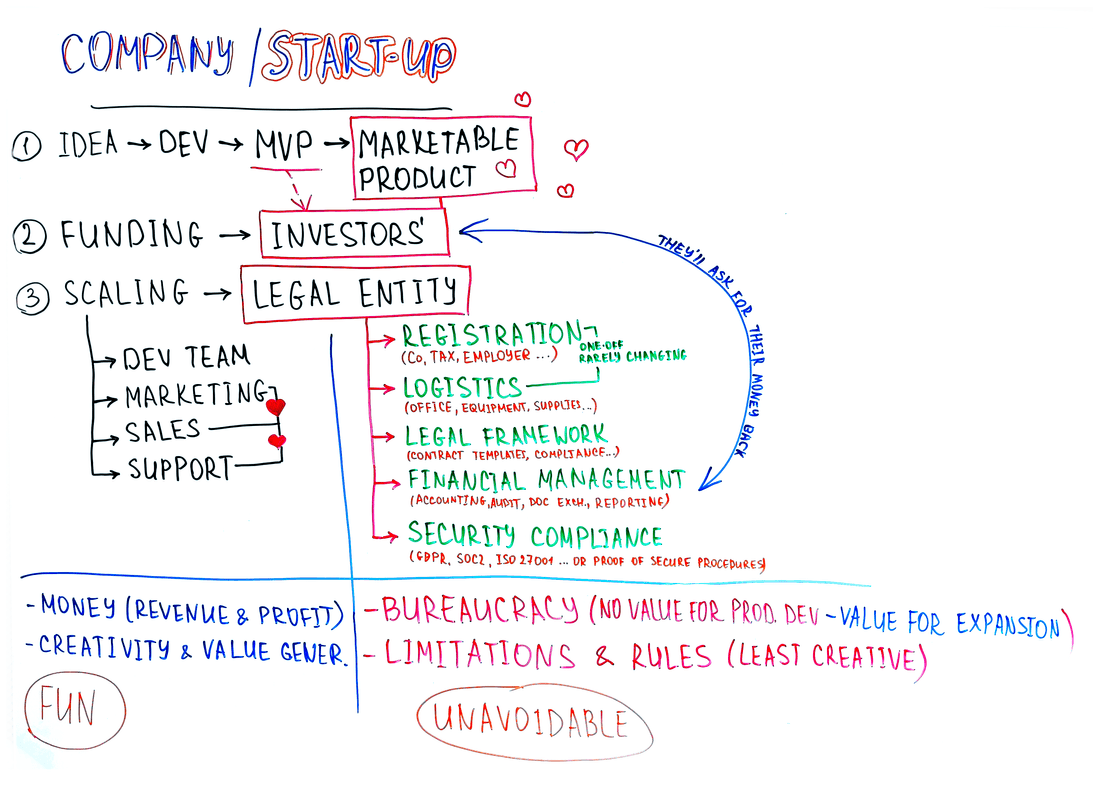

If we combine product, marketing, operational and legal needs of a startup and lay it out as a scheme it will look somewhat like this:

After enduring months, all the regulations and legal formalities are over, and you can just keep working! You feel enthusiastic and are determined to dedicate 100% of your attention to what truly matters - your product and market expansion.

I’m sorry to say this, but here is another part of the boring reality you have to face:

- Your accountant comes every month and reminds you to provide all invoices and receipts. They frighten you with penalties or legal issues if you fail to meet the requirements.

- Your bankers come every year to verify UBOs identities. You also need to provide the necessary documents due to the constantly changing regulations.

- Your investors expect regular reports on your expenses. They want to know your cashflow, your burn rate, review auditors’ reports, as well as an analysis of the planned versus actual financial status of your startup.

Just before you know it, you shift your attention from the product and drown in making sure that you satisfy all the stakeholders.

Fibery is not different. We have encountered the same challenges as everyone else. As a product company, we didn’t particularly enjoy getting involved in bureaucracy. However, every endeavour requires a process, and it’s important to structure and develop it in a way that suits your business. Since our focus is on managing knowledge and processes, it made sense to utilize our own tool for financial reporting.

It all starts with a process.

How to set up financial operations in a product startup

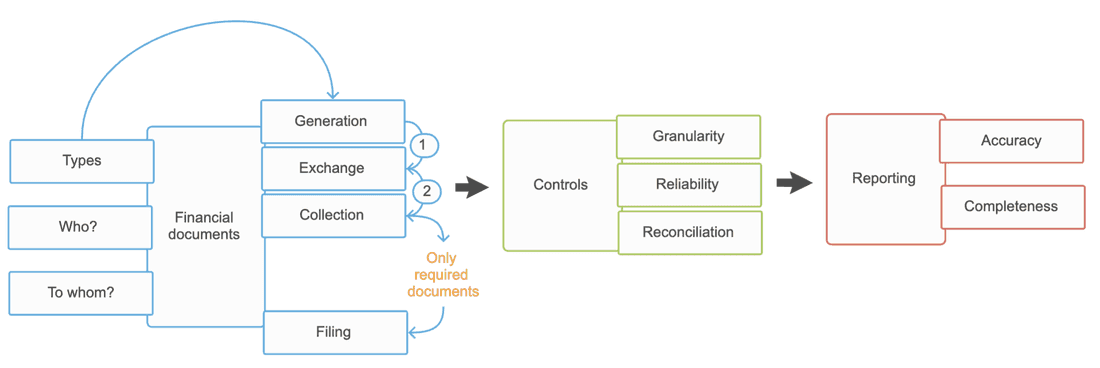

To set basic financial operations, or FinOps, you need to understand financial documents: how you generate, exchange, collect, control - and send them to your accountant.

We will guide you step by step.

Step 1- Understanding financial documents and workflow

- What financial documents do you have to process?

It varies on a specific business, but generally, the documents you need to store are the ones that justify money flow (both inflow and outflow). These are purchase invoices, insurance policies, contracts, subscriptions, sales invoices, and payroll documents.

- How are financial documents generated, exchanged, and collected?

- Who sends the documents and where?

- Who will be responsible for processing or approving them?

- Where will the final documents be saved?

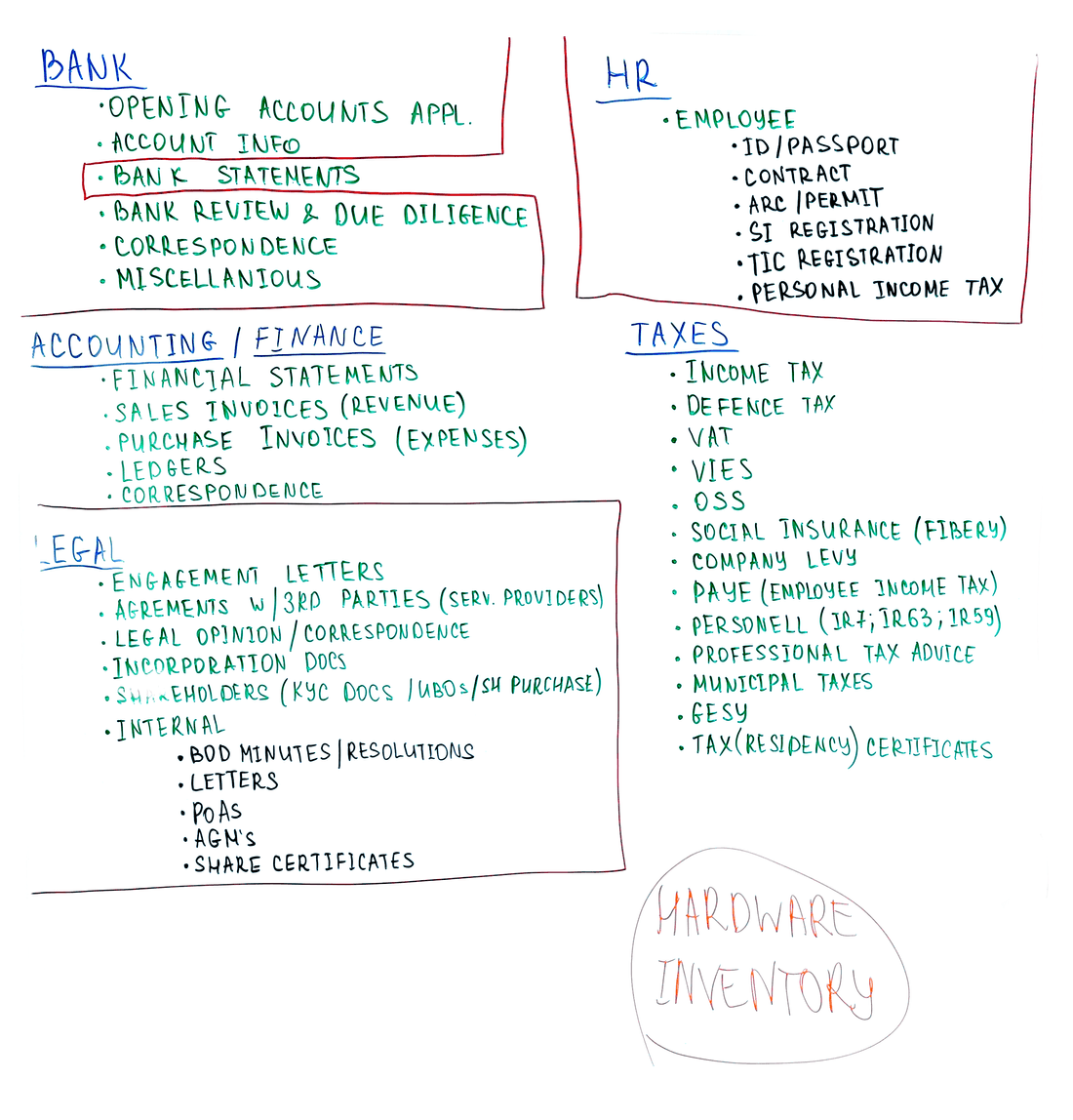

The original draft for Fibery, outlining the documents needed for managing financial operations, looked something like this:

It is not a structure “set-in-stone”. Bear in mind that once your business evolves, this structure will be reviewed and modified. It should be flexible enough to accommodate the ongoing changes.

Step 2 - Setting up financial controls

Now you are ready to set up controls.

The controls are policies or procedures put in place to manage or mitigate risks and ensure compliance with the regulations. They are designed to monitor, prevent, detect, and address potential issues. The controls will allow you to effectively ensure that you don’t miss anything when reporting to your accountants.

Here are the main questions you should ask yourself when establishing controls:

- Granularity: How deep would you like to be able to drill into your documents, both upwards and downwards? Would you like to see a list of documents based on counterparties, types of expenses, and the banks involved in the transaction?

- Reliability: How can you identify discrepancies in the data? How will you prevent errors when referring documents into specific categories such as expense or income type, legal entity type, and bank?

- Reconciliation: Reconciliation is the process of comparing your company’s bank statements to your own records, ensuring that all transactions are accounted for. Check whether every transaction has related document to justify it.

Unfortunately, reconciliation alone is not enough.

The majority of companies run their accounting on an accrual basis. This means that revenue or expenses are recorded when they are earned or incurred, regardless of when the cash is received or paid.

Plainly speaking, any document you receive should be recorded and reported as an expense or revenue, regardless of the actual money received or paid.

There are delayed liabilities and delayed payments. Delayed liabilities occur when goods or services have already been provided, but the payment is scheduled for the future. Delayed payments, on the other hand, happen when a company provides services or goods but receives the payment at a later date.

The bulletproof method for control here is checking the outstanding balances per counterparty. This involves checking if each document has a corresponding bank transfer or if there is any remaining outstanding amount. Accountants call it a statement of account.

Step 3 - Setting up reporting

Once you have your controls in place and your documents are ready, you can report to your accounting department.

Here are the main principles your reporting needs to adhere to:

- Accuracy. The controls should ensure that 99% of the documents are in place. We always allow for 1% error, and we are working on eliminating such possibilities to zero.

- Completeness. The controls mentioned above should allow you to spot documents that were not reported in the previous period and that you include in the current reporting period. This accounts for the 1% mentioned earlier.

All in all, structure, process and precision are all it takes to make sure that your accounting has everything it needs to work its magic with the rest of pretty messy bookkeeping.

Sounds like a hell of a lot of work, I agree. In the second part, I’m talking about one of the fundamental requirements - how to ensure you have all your paperwork in order.

Psst... Wanna try Fibery? 👀

Infinitely flexible product discovery & development platform.

More gems from our Radically Honest Blog:

Fibery in 2024. Year in Review

Tl;dr: 280 new paid customers (and 530 total) ❤️. 450 new features and 1400 fixed bugs 💪. 51 new releases 🌶️. Some failures (AI, Product teams strategy) 😱. Some wins (back to roots, your company's operating system focus) 🎢. Dopamine and cortisol 😍😨.

#54 Fibery.io in the First Half of 2024

Eight months have passed since the last Fibery digest, and it's time to reflect on the past and share future plans. From narrowing down core use cases to re-positioning Fibery as a no-code product discovery & development platform

Fibery 2.0 — Product Discovery & Development Platform That Answers Your Questions

If Fibery wasn't your top choice as a PM, it definitely will be from now on. Analyze user feedback & market signals, identify top insights, and unite discovery with development: this is Fibery 2.0